The growth you want—without all the work.

Demonstrate your value with CountingWorks PRO. Our AI-powered marketing automation platform empowers you to reshape the client experience from end to end.

All-In-One Practice Marketing Platform

The easiest way to build, grow, and run your firm.

.jpg)

How it works

One platform that does it all.

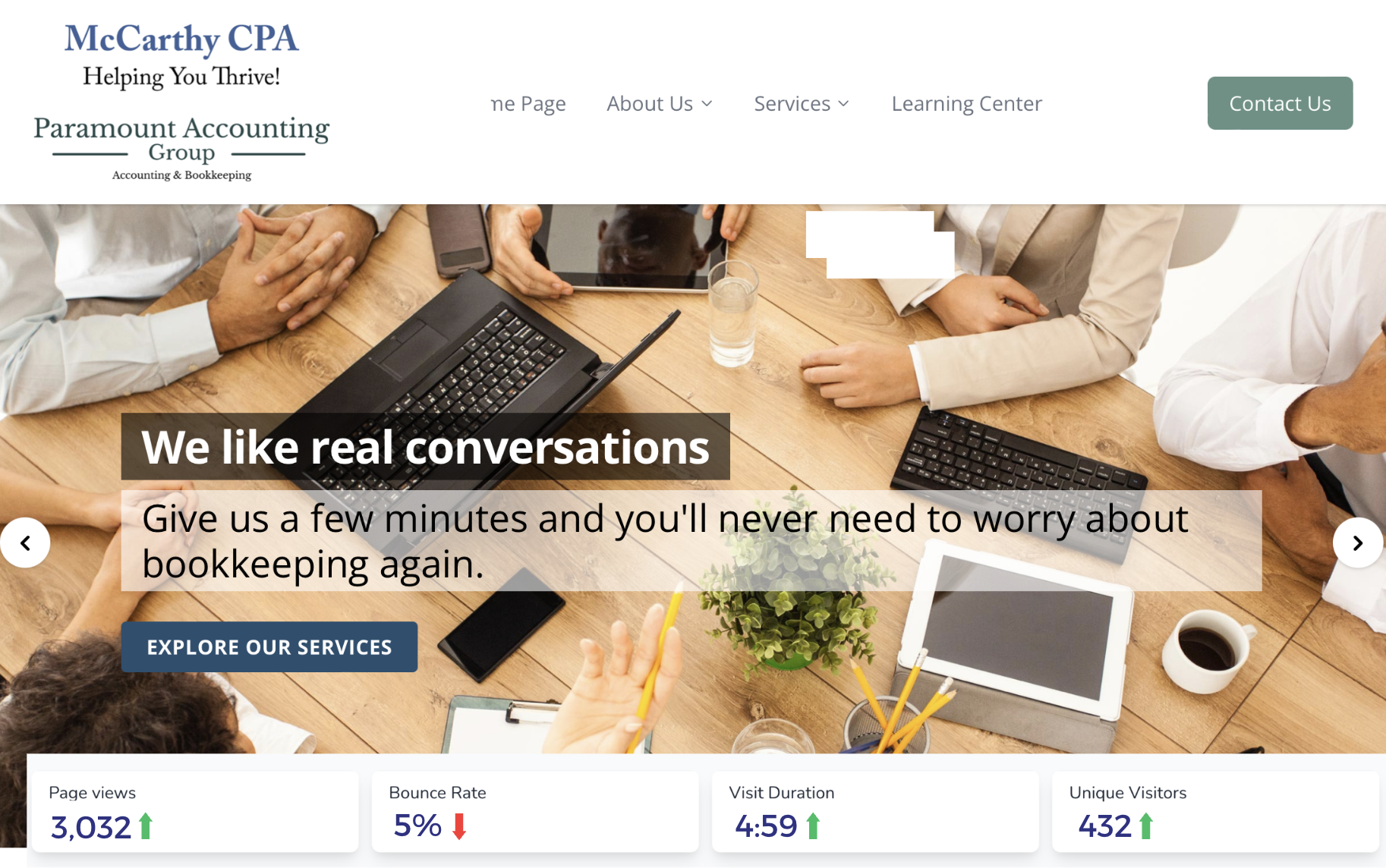

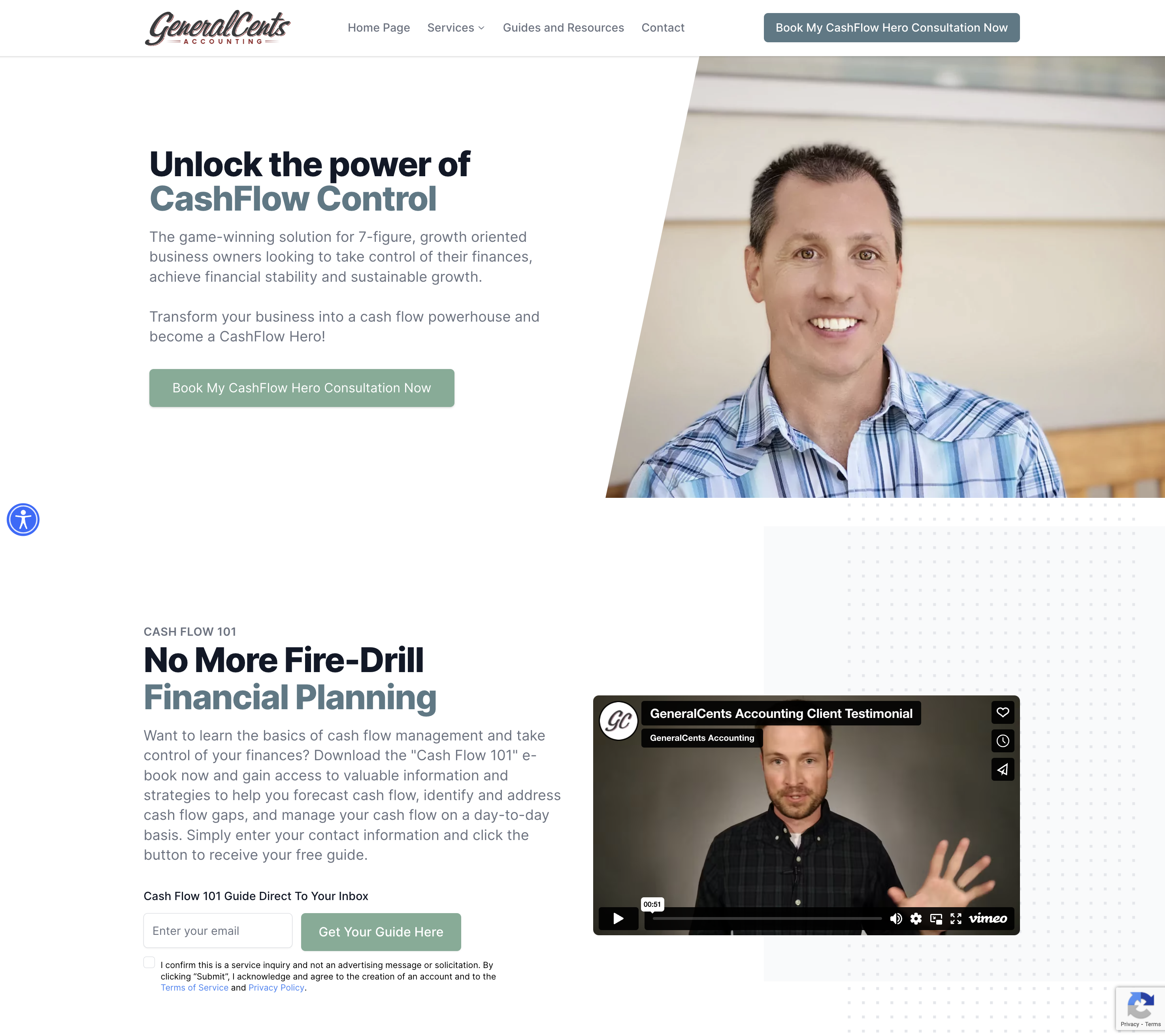

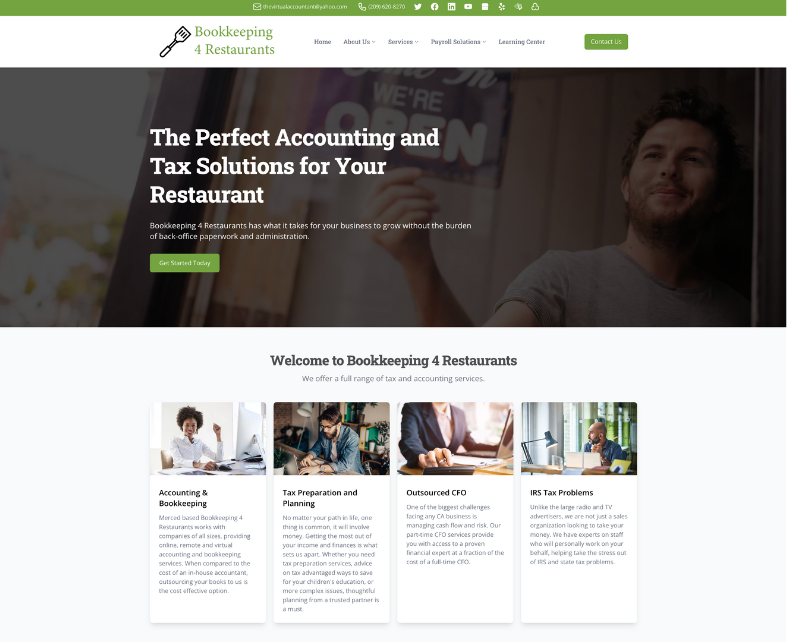

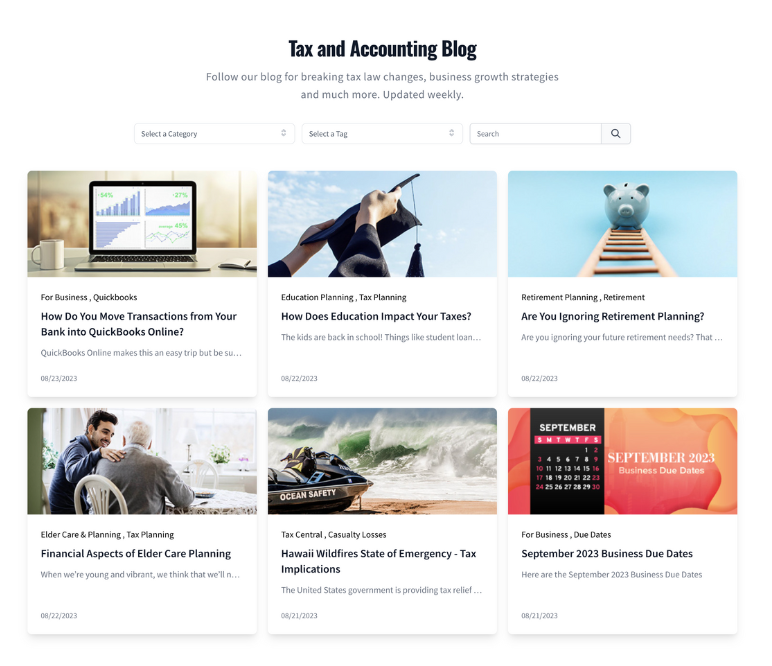

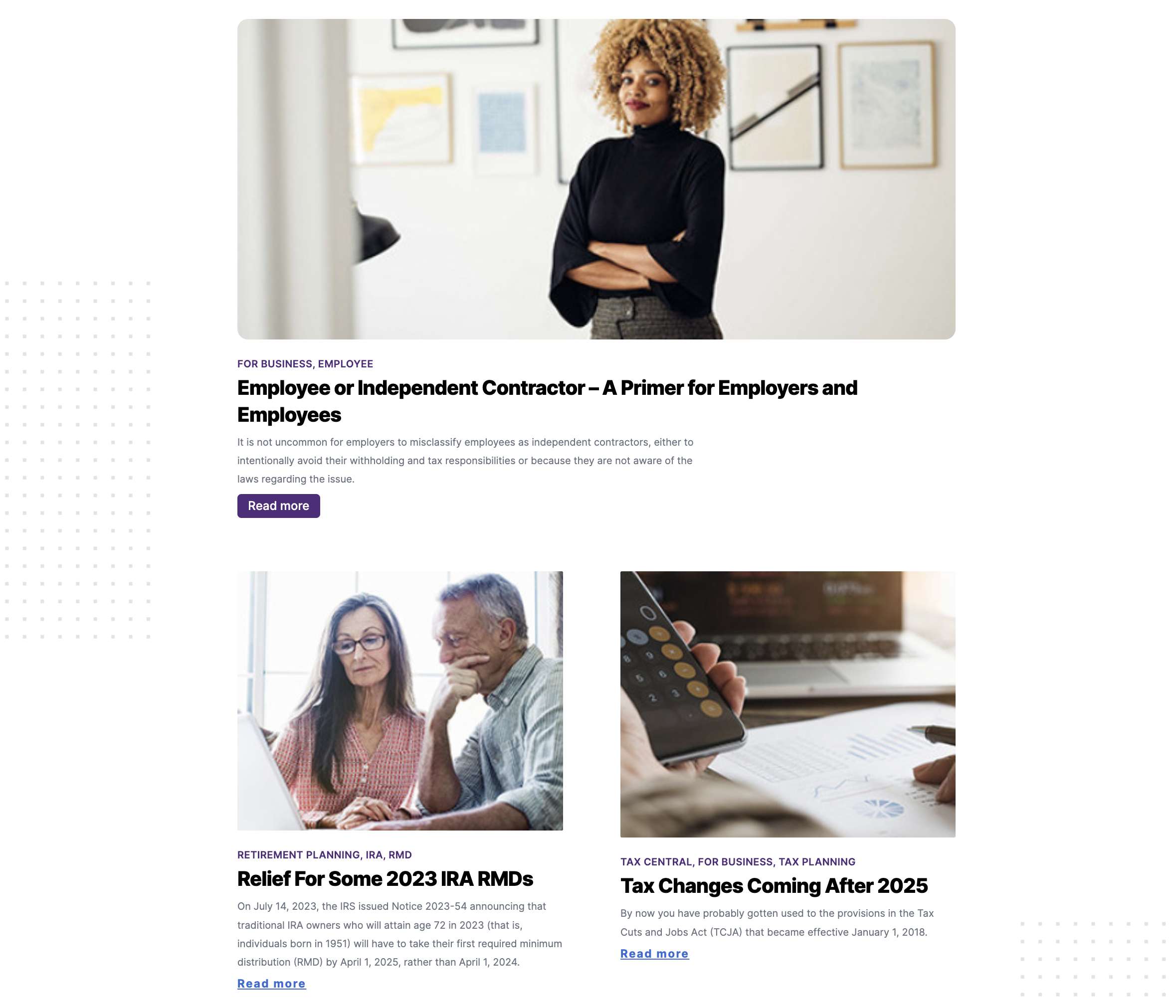

Get found online

Showcase your firm with a search engine optimized website, built just for you. Feed algorithms with engaging blog and social media content. Work with a marketing concierge to perfect your SEO, and outrank your competitors.

Track your website metrics in your dashboard.

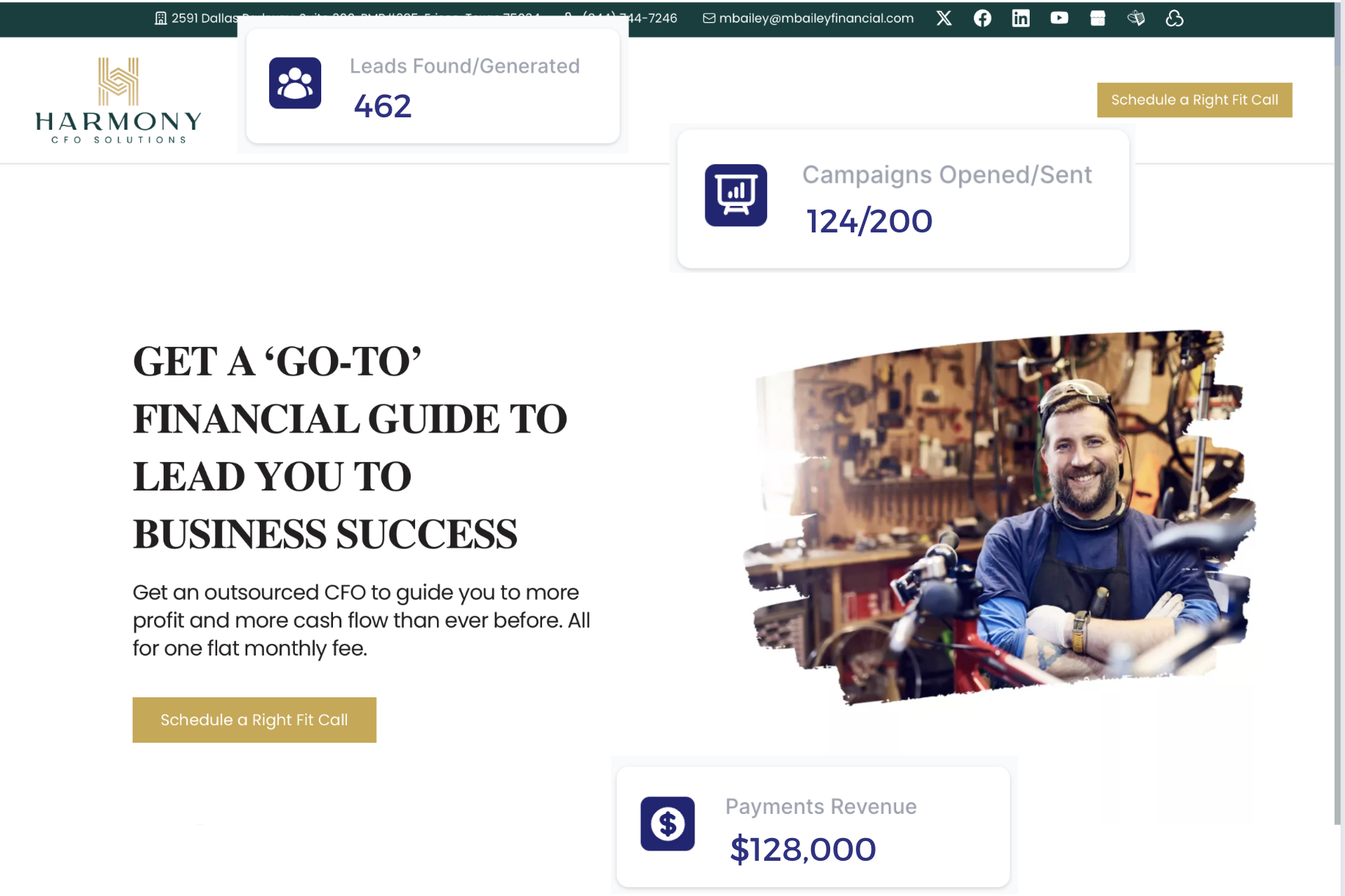

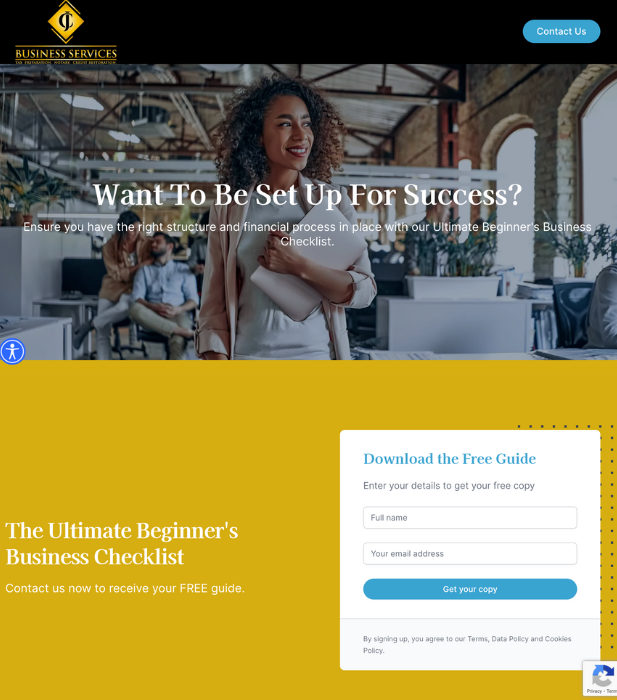

Convert and upsell prospects

Utilize our lead generation options, from landing pages and white papers to customizable lead forms and lead nurture campaigns, to convert prospects into clients. Double your revenue from existing clients with our 5-step upsell campaigns.

Lear more about client marketing

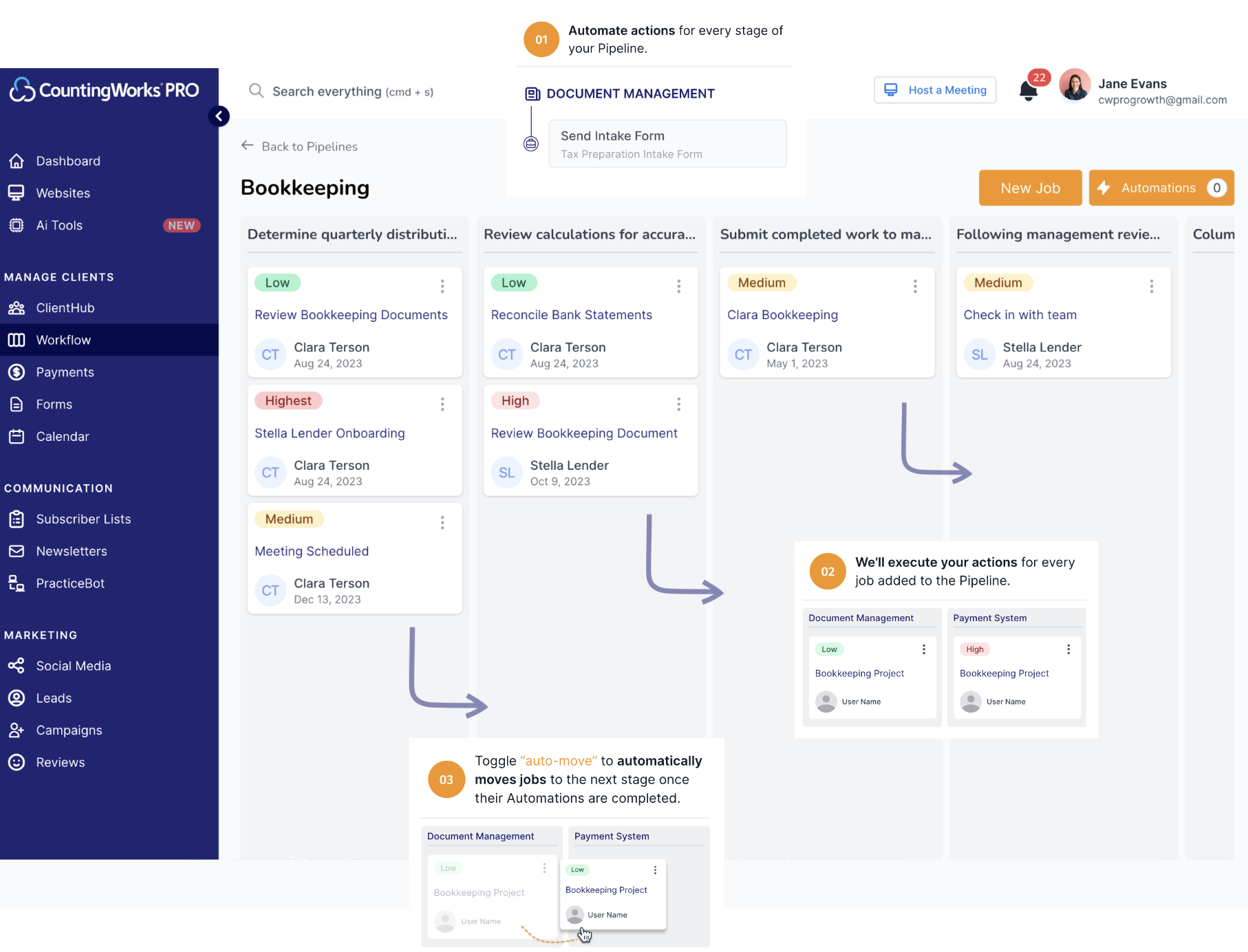

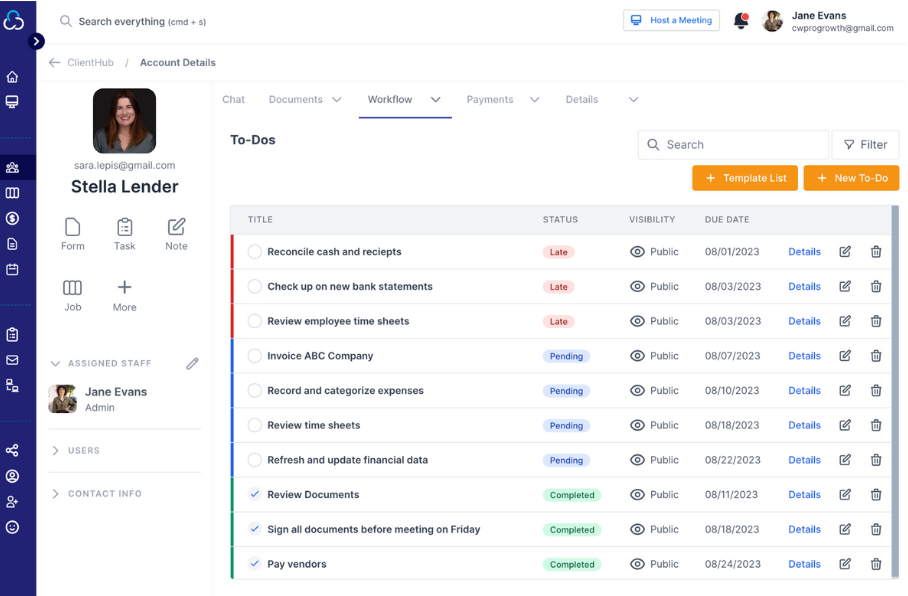

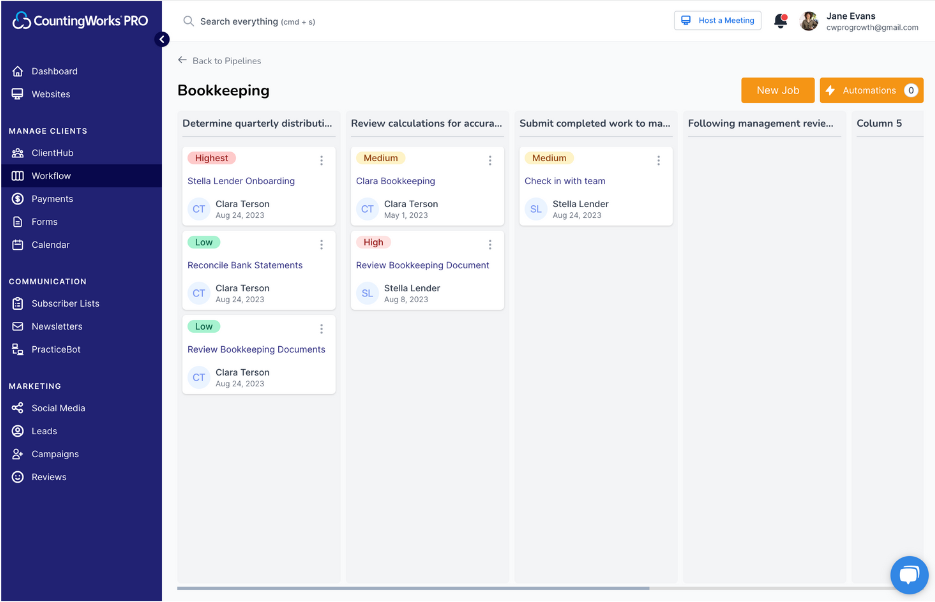

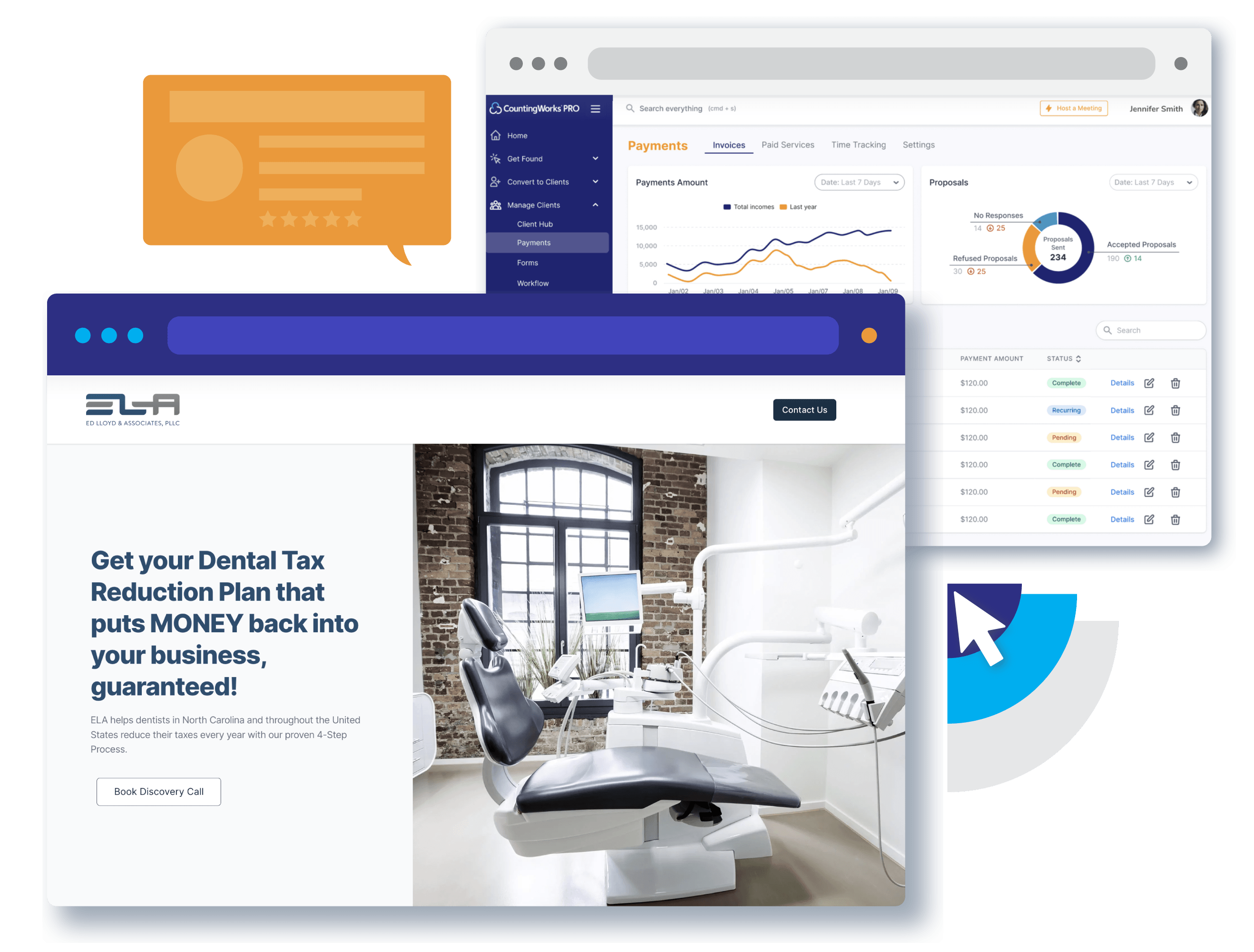

Save time on client work

Connect with your clients in a secure environment, with an intuitive user interface. ClientHub allows you to replace up to 10 other vendors including Calendly, TaxDome, Zoom, Docusign, Asana, and more.

Learn more about our ClientHub CRMWork smarter with AI

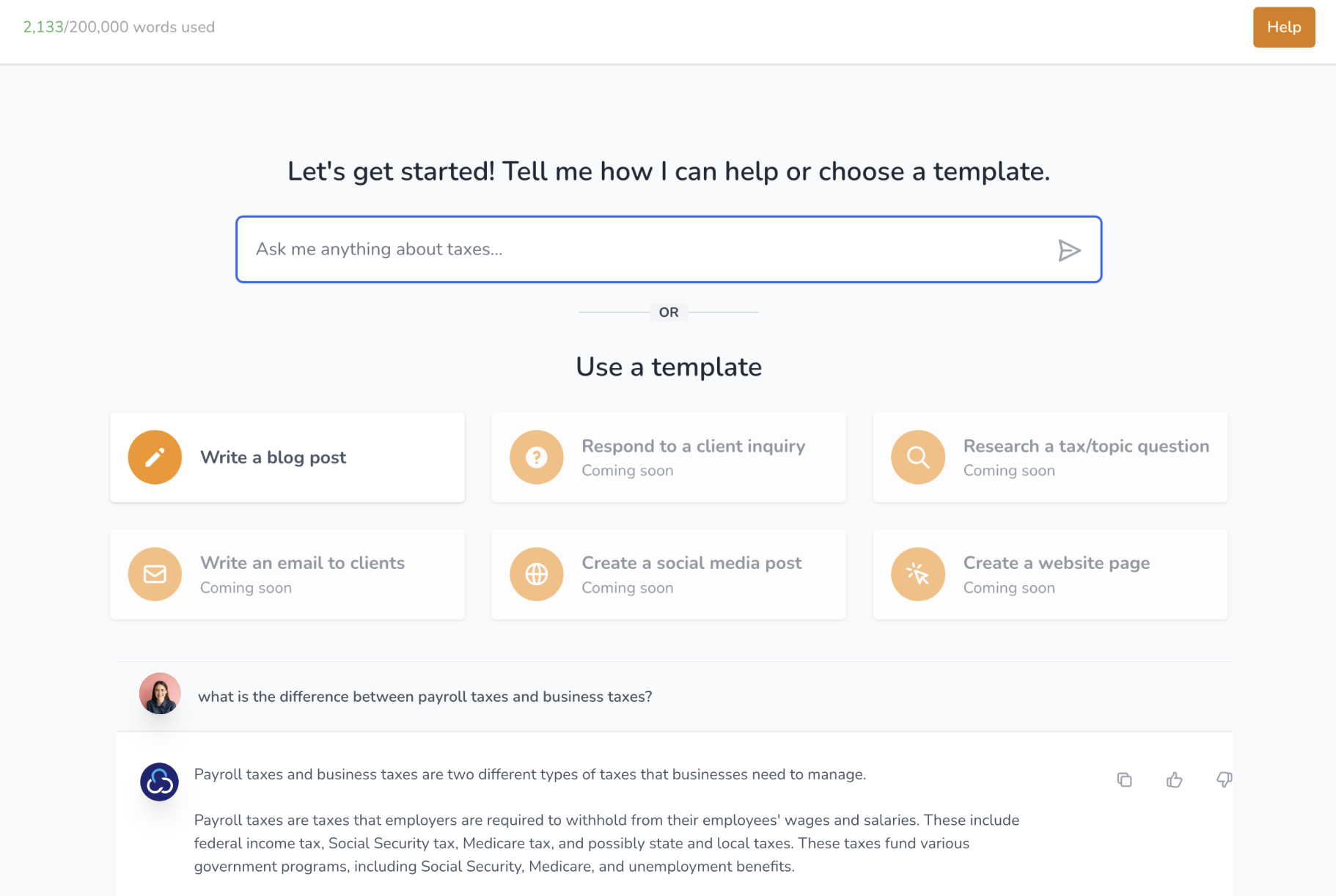

Use our powerful AI tools to streamline day to day tasks. Write blogs, create engagement letters, respond to client inquiries, or research tax topics in seconds.

Learn more about AI tools

Impacts seen by our clients

We are trusted by over 8,000 CPAs, Enrolled Agents, and Tax Professionals

10+

200 hours

$17,905

120%

200+

.png)

MARLENE VAN SICKLE, CPA

AUSTIN, TX CERTIFIED PUBLIC ACCOUNTANT

"The changes I have seen are great. I love that we can now push a password change for our clients... Thank you for your hard work at making the technology grow with the times. Well done."

See full review.png)

JOE CARLOZO

TIMONIUM, MD CERTIFIED PUBLIC ACCOUNTANTS

"I just wanted to say thanks for recognizing us in your Tax Buzz Top 100! Please know we are most appreciative of the recognition and feel honored..."

See full review.png)

R. WESLEY KIRTZ, CPA

WAYNESBORO, VA ACCOUNTING & TAX SERVICES

"We are getting daily prospects and several new clients per week. Whatever you are doing is working!"

.png)

RAFAEL CARMONA

PHOENIX, AZ SMALL BUSINESS ACCOUNTING

"I never thanked you for the great website. I am getting a lot of compliments. Thank you."

See full review.png)

CHRISTI BENDER, CPA

PHOENIXVILLE, PA TAX PREPARATION

"I've been getting a lot of compliments on the site. So, despite all the back and forth it came out wonderfully! Your picture selection, font, spacing and all the rest were fantastic. Thank you!"

.png)

LINDA ANGELES

CELEBRATION, FL TAX ACCOUNTING

"...Hiring a marketing director is costly and not worth it, so believe me when I say that CountingWorks PRO is the best thing to sliced bread! You can quote me on that too!"

.png)

KIM JUSTICE

ST. PETERSBURG, FL TAX & ACCOUNTING

"I have been getting so many referrals… thank you everyone at CountingWorks PRO."

What you get

Get Found

Build a beautifully branded website, and create your online presence with automated content marketing tools.

✓ Website Builder

✓ SEO Services

✓ Automated Social Media

✓ Review Collection Tools

✓ Multiple Site Management

✓ Automated Blog

✓ Curated White Papers

✓ AI Content Assistant

Convert Clients

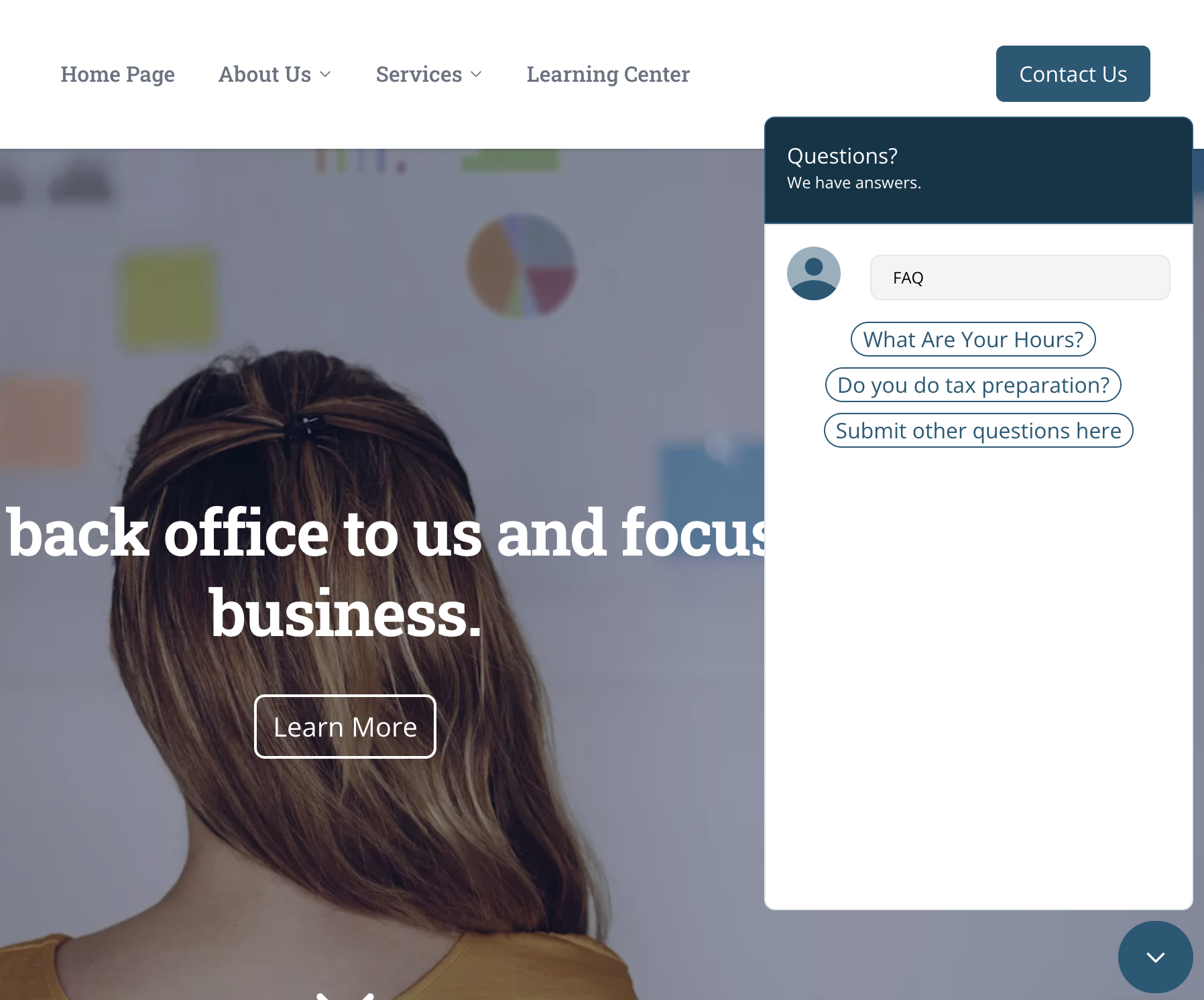

Turn web visitors into clients with lead generating landing pages, email campaigns, and an on-site chat bot.

✓ Lead Nurture Campaigns

✓ Lead Magnets

✓ FAQ Chat Bot

✓ Niche Landing Pages

Manage Clients

Manage all of your client work in one place, replace your extra software with one easy to use ClientHub.

✓ Client Portal

✓ Secure Private Chat

✓ Document Sharing

✓ Automated Workflows

✓ Time Tracking

✓ Video Meetings

✓ To-do List

✓ AI Tax Research

Retain Clients for Life

Keep your clients coming back for life, with retention marketing tools like our automated newsletters, and retention campaigns.

✓ Automated Newsletters

✓ Holiday Greetings

✓ Client Retention Campaigns

✓ Client Upsell Campaigns

We know there are other vendors out there.

See how we compare to our competition.

Advice in Your Inbox

Professional advice, ideas, and information to help your practice get going and grow.

Build, grow, and run your firm with CountingWorks PRO

.svg)